If you received an income tax notice under Section 143(2) in the last few weeks, you are not alone. Thousands of taxpayers across India, including many in Gurgaon and Delhi NCR, have received these notices in June 2026. There is a clear legal reason behind this sudden wave, and understanding it will help you respond calmly and correctly rather than in a panic.

This article explains what a Section 143(2) notice means, why so many are being issued right now, every common reason behind them, what happens if you ignore one, and exactly what to do when you receive one.

Why So Many Notices Are Coming Right Now

The Income Tax Department has a strict legal deadline to issue scrutiny notices for any assessment year. For returns filed for AY 2025-26, the last date by which a notice under Section 143(2) could be issued was 30th June 2026. As this deadline approached, the department’s automated systems ran through all filed returns, identified mismatches and concerns, and issued notices in bulk before the window closed permanently.

This happens every year. The department races against its own statutory deadline, and the result is a large number of notices going out in May and June of each year. If you received a notice recently, it almost certainly relates to your return for AY 2025-26, covering income earned in FY 2024-25.

The single most important thing to understand right away is this: receiving a scrutiny notice does not mean you have done something wrong. It does not mean the department has concluded that you evaded tax. It simply means your return has been selected for a closer look, and the department wants you to explain or document certain entries. Many completely honest taxpayers receive these notices every year and close them without any additional tax demand, simply by submitting the right documents with a clear, factual explanation.

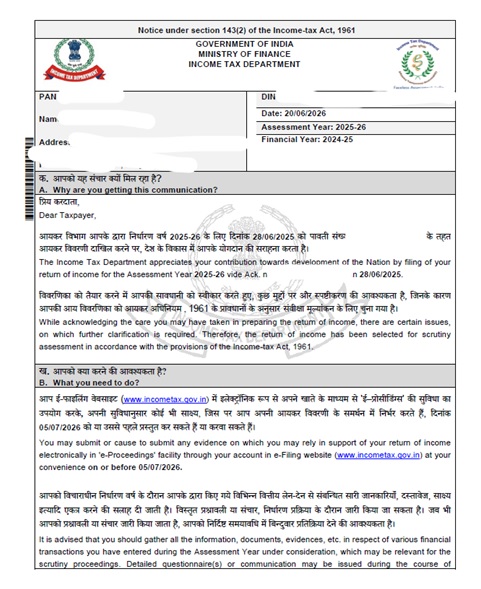

What Is a Section 143(2) Notice

A notice under Section 143(2) is issued when the Income Tax Department selects your return for detailed scrutiny assessment. The department examines whether you have correctly disclosed your income, correctly claimed deductions and exemptions, and paid the right amount of tax.

This notice is not the final outcome. It is the opening of an assessment process. After receiving the notice, the department will send a follow-up under Section 142(1) asking specific questions and requesting supporting documents. You submit your response with documents through the income tax portal. The Assessing Officer then reviews everything and issues a final assessment order under Section 143(3), which either confirms your original return, raises an additional tax demand, or results in a refund if you overpaid.

The entire process is now conducted online through the Faceless Assessment Scheme. You do not need to visit any income tax office. All communication happens through the e-filing portal, and notices are sent to your registered email address and mobile number simultaneously.

Two Types of Scrutiny: Limited and Complete

In limited scrutiny, the department examines only specific issues clearly mentioned in the notice, such as a particular income mismatch, a high-value transaction, or a specific deduction claim. The Assessing Officer cannot go beyond the stated points without prior approval from higher authorities. Most notices in the current wave are limited scrutiny notices, focused on one or two specific issues flagged by the automated system.

In complete scrutiny, the department reviews your entire return in detail, including every head of income, every deduction, every exemption, and all supporting disclosures. Complete scrutiny cases are significantly rarer and are reserved for returns where the department has identified more serious or widespread concerns.

How the Department Selects Returns for Scrutiny

The department uses an automated system called CASS, which stands for Computer Assisted Scrutiny Selection. CASS does not read returns manually. It compares the figures in your ITR against data it already holds from banks, credit card companies, mutual fund registrars, property registrars, employers, GST filings, and dozens of other institutions. When the numbers do not add up, the system flags the return and a scrutiny notice is generated. The following are the most common triggers behind the current wave of notices.

Trigger 1: Credit Card Spending Far Higher Than Declared Income

Banks report total annual credit card payments to the income tax department through the Statement of Financial Transactions. If your total credit card spend during the year was Rs 18 lakh or Rs 20 lakh, but your ITR shows income of only Rs 3 lakh or Rs 4 lakh, the system immediately raises a flag. Someone spending Rs 20 lakh on a credit card while earning Rs 4 lakh on paper presents an obvious question.

The explanation is often legitimate. The money may have come from savings built over previous years. A family member may be paying the credit card bill. The expenses may include business costs reimbursed by an employer. But the system has no way of knowing this without your explanation, which is why the notice is issued. Taxpayers whose lifestyle expenses visible in AIS are significantly higher than their declared income are among the most frequently flagged in the current wave.

Trigger 2: Fixed Deposit Investments Far Higher Than Declared Income

If your AIS shows that you opened or renewed fixed deposits worth Rs 50 lakh during the year but your ITR shows total income of only Rs 5 lakh, the department’s system asks an obvious question: where did Rs 50 lakh come from?

The answer may be entirely innocent. The money may have come from savings accumulated over many years, from an inheritance, from the maturity of an earlier investment, from a property sale in a previous year, or from a joint account with a spouse. But none of this is visible to the department without documentation. A notice is issued to ask for the explanation and the supporting evidence that goes with it.

Trigger 3: Investments in Shares and Mutual Funds Far Higher Than Declared Income

This is the most widespread trigger among retail investors right now. Many people invest regularly in mutual funds through monthly SIPs and make additional lump sum investments during the year. When the AIS shows total investments of Rs 80 lakh in shares and mutual funds but the ITR shows income of only Rs 12 lakh, a notice almost certainly follows.

The Rs 80 lakh figure in AIS may not represent fresh money at all. It may include mutual fund switches, where units from one scheme are moved to another and the registrar reports both the redemption and the fresh investment as separate transactions. It may include reinvestment of redemption proceeds from earlier investments. It may include investments funded from the sale of property or other assets that were declared as capital gains in the ITR. Or it may include investments made jointly with a spouse where both PAN numbers are tagged to the same transaction.

All of these are valid explanations, but they need to be presented clearly with supporting documents. A consolidated account statement from CAMS or KFintech, along with capital gains reports and source of funds documentation, is typically what is needed in response.

Trigger 4: Income Appearing in AIS but Missing from ITR

This is the most direct and straightforward trigger of all. If income appears in your AIS but is not declared in your ITR, the mismatch is flagged immediately. This commonly includes savings bank account interest that was not declared, fixed deposit interest that was overlooked, dividend income from shares that was not reported, rent received that was not included, or professional fees received where the client deducted TDS under Section 194J but the corresponding income was left out of the return.

The department now has complete visibility into this data from third-party sources. Any income reported by a bank, employer, or institution that does not appear in the return will be caught by the system without fail.

Trigger 5: Using the Wrong Presumptive Scheme

This trigger has become increasingly common as more professionals and small business owners opt for presumptive taxation, and the department’s system is now specifically checking for it.

Section 44AD applies to small businesses, and the deemed income is 6 or 8 percent of turnover. Section 44ADA applies specifically to specified professionals such as doctors, lawyers, engineers, architects, chartered accountants, and technical consultants, and the deemed income is 50 percent of gross receipts. These are two entirely separate provisions with very different income rates.

The problem arises when a taxpayer uses the wrong one. A doctor or consultant filing under Section 44AD instead of Section 44ADA declares income at only 6 or 8 percent of receipts instead of the required 50 percent. The system sees a professional’s gross receipts in AIS alongside a return declaring a tiny fraction of those receipts as income, and a scrutiny notice follows.

The reverse also causes problems. A trader or small business owner filing under Section 44ADA, which is not available to them since their income is not from a specified profession, makes an entirely invalid claim. Both errors result in notices, and both require professional assistance to address correctly.

Trigger 6: Filing the Incorrect ITR Form

Using the wrong ITR form is a direct trigger for scrutiny. The most common version is a taxpayer filing ITR-1 when their income situation required ITR-2 or ITR-3.

ITR-1 is available only to resident individuals with salary or pension income, income from up to two house properties, interest and other simple income, and total income up to Rs 50 lakh, with no capital gains beyond the small LTCG threshold now permitted under the relaxed eligibility. A taxpayer who has capital gains from shares or property, holds foreign assets such as ESOPs from a foreign parent company, is a director in a company, holds unlisted shares, or has business income on the side cannot use ITR-1. Filing ITR-1 in these situations means entire heads of income are simply absent from the return, since the relevant schedules do not exist in that form.

Another version is a freelancer or self-employed professional filing ITR-4 when their income profile actually requires ITR-3, for example because gross receipts have crossed the presumptive threshold, or because capital gains or other complex income cannot be accommodated in ITR-4.

The department’s system compares the form filed against the full income profile visible in AIS. Where they are inconsistent, a notice follows. Incorrect ITR form selection is one of the explicitly listed triggers in the CASS parameters.

Trigger 7: Incorrect or Inflated Deduction Claims

Deduction claims that are disproportionate to income declared, or that cannot be verified against third-party data, are a well-established trigger. The system does not need to examine documents to flag this. It simply looks at whether deduction amounts are unusual relative to the income level, or whether the taxpayer has made significantly larger deduction claims than in previous years without a visible reason.

Specific deductions that frequently attract scrutiny include Section 80C claims at exactly the maximum of Rs 1.5 lakh every year regardless of actual investments, Section 80D health insurance premium claims without matching data from insurance companies, HRA exemption claimed for periods when the rent payments cannot be traced through banking channels, home loan interest claimed under Section 24(b) for a property that was under construction during the year, and Section 80G donations to organisations whose registration has lapsed or cannot be verified.

The department cross-references deduction claims against data from insurance companies, banks, and other institutions. Claims that cannot be verified against this third-party data are routinely flagged. If you receive a notice about deductions, the response must be built entirely on actual documents, not on written explanations alone.

Trigger 8: Mismatch With AIS and Third-Party Data Sources

This is the broadest trigger and the one behind the most sophisticated scrutiny selections in the current wave. The income tax department now receives detailed data from an extensive network of third-party sources through the Statement of Financial Transactions. These include commercial banks reporting savings account interest, fixed deposit interest, and cash deposits above prescribed thresholds; mutual fund registrars reporting all purchase, redemption, and switch transactions; depositories reporting all share purchases and sales; property registrars reporting all property transactions; credit card companies reporting total annual spend; foreign remittance data from authorised dealers; GST network data for registered businesses and professionals; and employer payroll data through TDS returns.

What makes the current wave of scrutiny notices different from earlier years is that the system is now matching patterns across all of these sources simultaneously. A taxpayer whose combined data across credit cards, fixed deposits, share investments, and property transactions shows a financial profile significantly larger than the income declared in the ITR is flagged even if no single transaction individually would have triggered a notice. The department uses AI and data analytics to detect these patterns, which is why taxpayers who believe they have filed correctly are still receiving notices. The system is looking at the complete financial picture, not just one number.

The most effective protection against this trigger is reconciling your AIS fully before filing. Every entry should be matched against your own records, incorrect entries should be challenged through the feedback mechanism within AIS, and where entries are correct but need context, proactive documentation should be prepared in advance.

Trigger 9: GST Turnover Mismatch With ITR Income

For business owners and professionals who are registered under GST, the GST network reports aggregate turnover figures directly to the income tax department. These are matched against the turnover or gross receipts declared in the ITR. Where a business shows turnover of Rs 80 lakh in GST returns but declares only Rs 60 lakh in the ITR, the difference is flagged immediately.

Business owners who are GST registered should always reconcile their ITR gross receipts figure against their total GST turnover before filing, and be ready to explain any difference with documentation.

What Happens If You Ignore the Notice

Ignoring a Section 143(2) notice is never an option. The department will proceed to a best-judgment assessment under Section 144, where the Assessing Officer determines your income based solely on the information available to the department, without the benefit of your explanation or documents. This almost always results in a tax demand that is far higher than your actual liability, along with interest under Sections 234A and 234B and penalties. Recovering from a best-judgment assessment is significantly more difficult and expensive than responding to the original notice on time.

The notice will specify a deadline, generally 15 to 30 days. Always check the specific date printed on the notice rather than assuming a standard period, and treat that date as non-negotiable.

Step by Step: What to Do When You Receive This Notice

Step 1: Read the notice carefully. Identify the assessment year, the specific issue flagged, and the exact response deadline.

Step 2: Log into the income tax e-filing portal and go to Pending Actions, then e-Proceedings. Download the full notice and note your original ITR acknowledgement number.

Step 3: Pull up your AIS, Form 26AS, and original ITR for the relevant year. Match the specific entry the notice is questioning against your own records.

Step 4: Gather supporting documents. Depending on what is flagged, this may include bank statements, FD receipts, mutual fund consolidated account statements, broker capital gains reports, property sale documents, credit card statements, source of funds evidence, investment proofs, or deduction-related certificates and receipts.

Step 5: Prepare a clear, point-by-point, factual response addressing every issue raised in the notice. Every explanation must be supported by actual documents. A vague explanation or a claim of cash transactions without banking evidence will not be accepted and may worsen the outcome.

Step 6: Submit the response and all supporting documents through the e-Proceedings section of the portal before the deadline. Save the submission confirmation number.

Why Professional Help Makes a Real Difference

How a response to a scrutiny notice is drafted matters enormously. A well-prepared, documented, point-by-point response typically closes a limited scrutiny notice without any additional demand. A vague or incomplete response, or one that inadvertently raises new questions, can escalate the matter to a draft assessment order stage, which is significantly harder and more expensive to resolve.

A CA familiar with scrutiny proceedings knows which documents carry the most weight for each type of trigger, how to address a source-of-funds query without opening new lines of inquiry, how to frame an explanation in the language the Faceless Assessment Unit expects, and when to push back on an AIS entry versus when to accept and explain it. For anyone who has received a notice in the current wave, getting professional guidance before submitting the response, rather than after a draft assessment order has already been issued, is the single most practical step available.

Disclaimer:

The information contained in this article is intended for general informational and educational purposes only and does not constitute legal, tax, accounting, or professional advice. While every effort has been made to ensure the accuracy and completeness of the information, laws, regulations, and judicial interpretations are subject to change and may vary depending on the specific facts and circumstances of each case.

Readers are advised to consult a qualified professional before taking any action based on the contents of this article. Neither the author nor Nitin Bhatia & Associates shall be liable for any loss or damage arising from reliance on the information provided herein.

Suggestions, corrections, and feedback are always welcome. If you believe any update, clarification, or modification is required, your valuable inputs are invited and appreciated.