The introduction of the Income-tax Act, 2025 marks a significant shift in India’s tax framework. With a focus on simplification, clarity, and ease of compliance, the new Act aims to make return filing more structured and taxpayer-friendly. As we move towards filing Income Tax Returns (ITR) for Tax Year 2026–27 (income of FY 2026–27), it is important to understand the timelines, provisions, and procedural changes introduced under the new law.

Availability of ITR Forms for Tax Year 2026–27

One of the first concerns for taxpayers each year is the availability of ITR forms. Under the Income-tax Act, 2025, the ITR forms will be notified under the Income-tax Rules, 2026. The Government is expected to release these forms well before the due dates for filing returns, ensuring that taxpayers have sufficient time to comply.

Once notified, the forms will be made available on the official e-filing portal. The objective is to ensure a smooth and timely filing process, minimizing last-minute challenges. Taxpayers are advised to keep track of updates and begin preparing their financial data in advance.

Time Limits for Filing Different Types of Returns

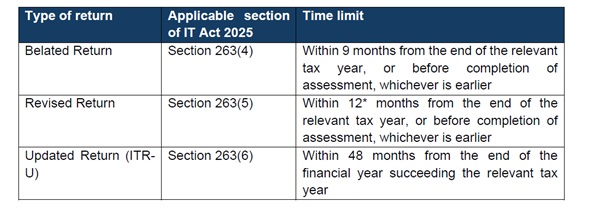

The new Act introduces clear timelines for filing various types of returns, including belated, revised, and updated returns. These timelines are designed to promote timely compliance while still offering flexibility to taxpayers who may need to make corrections or disclosures later.

A belated return can be filed within 9 months from the end of the relevant tax year or before the completion of assessment, whichever is earlier. This provides an extended window for taxpayers who miss the original due date.

A revised return, which allows correction of errors or omissions in the original return, can be filed within 12 months from the end of the relevant tax year or before completion of assessment. This extended period (as proposed in the Finance Bill, 2026) offers taxpayers additional time to ensure accuracy in reporting.

An updated return (ITR-U) can be filed within 48 months from the end of the financial year succeeding the relevant tax year. This provision enables taxpayers to voluntarily disclose additional income even after the expiry of the belated and revised return timelines.

Source: Incometaxindia.gov.in

Key Provisions of Updated Return (ITR-U)

The concept of updated return continues under the new Act with certain important conditions. It provides an opportunity for taxpayers to rectify omissions or declare additional income voluntarily, thereby promoting voluntary compliance.

An updated return can be filed regardless of whether the taxpayer has filed an original, belated, or revised return. However, only one updated return is allowed per tax year, ensuring that the provision is not misused.

It is important to note that an updated return cannot be filed to declare a loss, reduce tax liability, or claim a higher refund. The intent is to allow only upward revision of income and tax liability.

Additionally, taxpayers are required to pay additional income tax under the prescribed provisions along with the updated return. This acts as a deterrent against delayed disclosures while still offering a compliance window.

Overall, the updated return mechanism under the new Act is largely similar to the earlier provisions but continues to play a crucial role in encouraging transparency and compliance.

Return Filing in Case of Search Proceedings

The transition from the old Income-tax Act, 1961 to the new Income-tax Act, 2025 raises questions regarding ongoing proceedings, particularly in cases involving search and seizure.

If a search is initiated under the provisions of the old Act before the new Act comes into effect, all related proceedings will continue to be governed by the old law. Even if the notice for filing return for the block period is issued after 1 April 2026, the provisions of the Income-tax Act, 1961 will apply.

For instance, if a search operation is conducted in January 2026, all assessments and proceedings arising from that search will be carried out under the old Act. The taxpayer will be required to file returns as per the provisions applicable under the earlier law.

This ensures continuity and avoids confusion or legal complications arising from the transition between the two Acts.

Requisition Cases under the Old Act

Similarly, in cases where books of account, documents, or assets have been requisitioned under the provisions of the old Act before the new Act comes into force, all subsequent proceedings will continue under the old law.

This means that any follow-up actions, assessments, or compliance requirements related to such requisitions will be governed entirely by the Income-tax Act, 1961. The new Act will not have any impact on these ongoing proceedings.

Final Words

The Income-tax Act, 2025 brings a more structured and simplified approach to return filing for Tax Year 2026–27. With clearly defined timelines for belated, revised, and updated returns, along with continued provisions for voluntary compliance through updated returns, the new law aims to reduce complexity and improve transparency.

At the same time, the government has ensured a smooth transition by allowing ongoing search and requisition cases to be governed by the old Act. This balance between reform and continuity is crucial for maintaining stability in the tax system.

As taxpayers prepare for the upcoming filing season, staying informed about these changes will be key to ensuring accurate and timely compliance.