The Income-tax Act, 2025 will come into effect from 1st April 2026. Many taxpayers are confused about how this change will impact their pending refunds, excess TDS claims and income tax return filing. The good news is that the government has ensured a smooth transition so that taxpayers do not lose their rights or face unnecessary difficulties.

In this blog, we explain everything in simple language so you can clearly understand how the old and new laws will work together.

What Happens to Pending Refund Claims

One of the biggest concerns is whether refund claims under the old law will still be valid after the new Act starts.

The law clearly provides that all rights and benefits under the Income-tax Act, 1961 will continue even after the new Act comes into force. This means if you were eligible for a refund for any earlier year, your claim will remain valid and will be processed accordingly.

In simple terms, your refund will not be cancelled just because the new law has started. It will continue under the old provisions.

Refund of Excess TDS Deducted

Many taxpayers face situations where excess TDS is deducted. A common question is whether such refunds can still be claimed after April 2026.

The answer is yes. You can still claim the refund even after the new Act comes into force. However, you must follow certain conditions. The claim must be filed within two years from the end of the financial year in which TDS was deducted. The application should be filed in Form 26B and it will be processed under the old Income-tax Act, 1961.

This ensures that taxpayers do not lose their money due to technical changes in law.

Return Filing System Under Income-tax Act, 2025

The new Act introduces a simplified structure for filing returns. All types of returns such as original return, belated return, revised return and updated return are now covered under one section, which is Section 263.

However, the overall system remains the same. The categories of taxpayers who need to file returns, the due dates and the basic process continue as before. This means taxpayers will not face any major changes in compliance.

Due Dates for Filing Income Tax Returns

The due dates for filing income tax returns remain unchanged under the new Act. Individuals who are not subject to audit will file their returns by 31st July. Businesses not requiring audit will file by 31st August. Companies and audit cases will have a due date of 31st October, while certain special cases will have a due date of 30th November.

Since there is no change in deadlines, taxpayers can continue following the same timeline as earlier.

Detailed Due Date Table

| Category of Taxpayer | Conditions | Due Date |

| Individuals (non-audit cases) | Normal taxpayers | 31st July |

| Business/Profession (non-audit) | Not subject to audit | 31st August |

| Companies & Audit Cases | Audit required | 31st October |

| Special cases (e.g., shipping business u/s 172) | Specific conditions apply | 30th November |

Which Law Will Apply During Transition

This is the most important concept to understand. The applicable law depends on the period in which the income is earned and not on the date of filing the return.

If the income is earned before 1st April 2026, the old Income-tax Act, 1961 will apply. If the income is earned on or after 1st April 2026, the new Income-tax Act, 2025 will apply.

In simple words, income of earlier years will continue to be governed by the old law even if the return is filed after the new law comes into force.

ITR Filing for FY 2025–26

The financial year 2025–26 is a transition period. Even though the return for this year will be filed after 1st April 2026, it relates to income earned before the new law starts.

Therefore, the return for Assessment Year 2026–27 will be filed under the Income-tax Act, 1961. The same ITR forms such as ITR-1, ITR-2, ITR-3 and others will continue to be used.

Revised Return Rules

If you have made any mistake in your return, you can file a revised return. For Assessment Year 2026–27, the revised return can be filed up to 31st March 2027 or before completion of assessment, whichever is earlier.

Even if you revise the return after April 2026, the old law will continue to apply since the income relates to an earlier period.

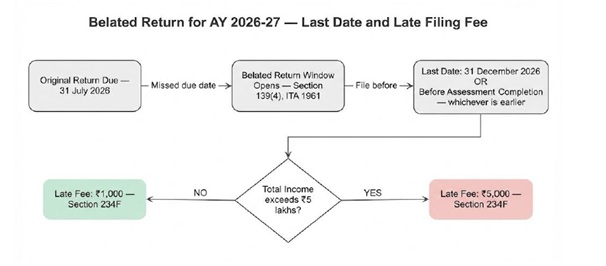

Belated Return and Late Filing Fees

If you miss the original due date, you can still file a belated return. For Assessment Year 2026–27, the belated return can be filed up to 31st December 2026.

However, late filing fees will apply. If your income is up to five lakh rupees, the fee will be one thousand rupees. In other cases, the fee will be five thousand rupees.

Updated Return Option

The option to file an updated return also continues. Even after the new Act comes into force, you can file an updated return for earlier years under the old law, subject to the prescribed time limits.

For example, if you filed your return in 2026 and later discover additional income in 2028, you can still file an updated return for that year under the old provisions.

Filing Returns for Earlier Assessment Years

For assessment years up to 2025–26 or earlier, the time limit to file revised or belated returns will expire before 1st April 2026. Therefore, such returns cannot be filed after the new Act comes into force.

However, taxpayers can still file an updated return for those years if they are within the allowed time limit.

ITR Forms After Implementation of New Act

Even after the new law is implemented, the old ITR forms will continue to be used for earlier assessment years. The income tax portal will support filing for past years, ensuring that taxpayers do not face any issues.

This continuity makes the transition smooth and practical.

Final Words

The introduction of the Income-tax Act, 2025 is a significant reform, but it does not negatively impact taxpayers for past years. All rights such as refunds and TDS claims remain protected, and the old law continues to apply to income earned before April 2026.

Taxpayers should focus on understanding which law applies to their income and ensure timely and correct filing of returns. Proper compliance will help avoid penalties and ensure smooth processing of refunds.