Introduction

With the transition to the Income-tax Act, 2025, taxpayers must clearly understand how self-assessment tax payments and carried forward MAT/AMT credits will be treated. While the new law introduces structural and terminological changes, the fundamental principles governing tax payments and credit availability continue largely unchanged. The key lies in understanding how the transition between the old and new Acts will operate in practical scenarios.

Self-Assessment Tax: Which Law Applies?

A common question arises regarding the applicability of law when self-assessment tax is paid after the new Act comes into force. It is important to understand that self-assessment tax is only a mode of discharging tax liability, and the applicable law depends on the year in which the income was earned, not the date of payment.

For example, if self-assessment tax for Assessment Year 2026–27 (Financial Year 2025–26) is paid in July 2026, it will still be governed by the provisions of the Income-tax Act, 1961. This is because the income relates to a period prior to 1st April 2026. Accordingly, the provisions of section 140A of the old Act will apply in such cases.

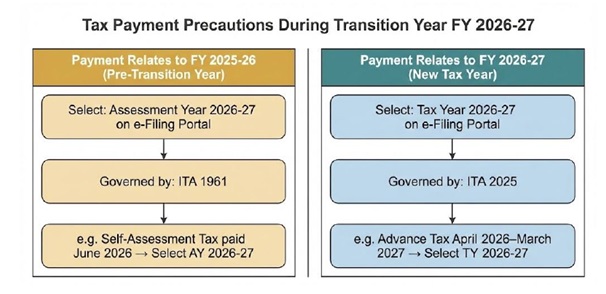

Precautions During the Transition Year

The transition phase (FY 2026–27) is crucial, as both the old and new laws will operate simultaneously. While the government is ensuring that the income tax portal supports both frameworks, taxpayers must exercise caution while making tax payments to ensure correct credit.

The most important precaution is the correct selection of the relevant year:

- For tax payments relating to FY 2025–26, taxpayers must select Assessment Year 2026–27

- For tax payments relating to FY 2026–27 onwards, taxpayers must select Tax Year 2026–27

For instance, if self-assessment tax for FY 2025–26 is paid in June 2026, the taxpayer must choose AY 2026–27. On the other hand, advance tax paid for income earned between April 2026 and March 2027 must be linked to Tax Year 2026–27.

Incorrect selection may lead to mismatch of tax credit, which can cause delays in processing or unnecessary notices.

Source: Incometaxindia.gov.in

Annual Information Statement under the New Act

The Annual Information Statement (AIS) will continue to exist during the transition period. For tax periods governed by the Income-tax Act, 1961 (up to AY 2026–27), AIS will remain applicable in its current form.

However, from Tax Year 2026–27 onwards, under the Income-tax Act, 2025, AIS will evolve into a new format known as Form No. 168. This represents a continuation and enhancement of the existing reporting system, ensuring better transparency and tracking of taxpayer information.

Treatment of MAT/AMT Credit under the New Act

Another important concern for taxpayers, especially companies and professionals, is the treatment of Minimum Alternate Tax (MAT) and Alternate Minimum Tax (AMT) credits carried forward under the old Act.

The new law provides clarity by ensuring that any unutilised MAT/AMT credit available under the Income-tax Act, 1961 will continue to remain valid under the Income-tax Act, 2025. These credits will be treated as eligible credits under the new Act and can be utilized in future years.

For example, if a taxpayer has MAT credit carried forward from AY 2024–25, such credit will still be available for set-off under the new Act, subject to prescribed conditions.

Carry Forward Period for MAT/AMT Credit

The carry forward period for MAT/AMT credit remains unchanged. Unutilised credits can be carried forward for a total period of 15 years from the year in which they first became available.

This means that even after the transition to the new Act, taxpayers can continue to utilize these credits for eligible tax years starting from 1st April 2026, provided they fall within the permissible time limit and meet the specified conditions.

Final Words

The provisions relating to self-assessment tax and MAT/AMT credit under the Income-tax Act, 2025 ensure continuity, clarity, and protection of taxpayer rights during the transition phase. While the applicable law depends on the year of income, taxpayers must be cautious about selecting the correct year while making payments to avoid mismatches.

The continuation of MAT/AMT credits and the evolution of the Annual Information Statement further demonstrate that the new Act is designed to modernize the system without disrupting existing benefits. With careful planning and awareness, taxpayers can smoothly navigate this transition and ensure accurate compliance.