Introduction

The introduction of the Income-tax Act, 2025 has brought a significant structural change in the way tax laws are presented in India. However, when it comes to Tax Deducted at Source (TDS) and tax payment mechanisms, the government has ensured continuity. The objective is not to change the compliance framework but to simplify and streamline the existing provisions, making them easier to understand and implement for taxpayers and professionals.

No Change in Core Tax Payment Obligations

Under the new Act, the fundamental obligation to pay income tax remains unchanged. Whether it is through TDS, TCS, advance tax, self-assessment tax, or regular assessment, the overall framework continues as it existed under the earlier law. This means taxpayers and deductors can continue following the same principles and compliance practices without any disruption.

The reform focuses on presentation and clarity, rather than altering the substance of tax payment responsibilities.

Modes of Tax Payment Remain Unchanged

The modes for remittance of taxes under the Income-tax Act, 2025 continue to be the same. Taxes are to be deposited through authorized banking channels, including electronic payment systems as notified by the Government from time to time. This ensures that the existing digital infrastructure and payment mechanisms remain intact, providing continuity and convenience to taxpayers.

Simplification of TDS Provisions under the New Act

One of the most notable changes in the new law is the simplification and consolidation of TDS provisions. Earlier, the Income-tax Act, 1961 contained multiple sections ranging from Section 192 to Section 194T dealing with different types of payments. Under the new Act, these have been consolidated into just two key sections:

- Section 392: Covers TDS on income under the head “Salaries”

- Section 393: Covers TDS on all other payments

This restructuring significantly reduces complexity and makes it easier for taxpayers and professionals to locate and apply the relevant provisions.

Tabular Format for Better Understanding

Section 393 of the Income-tax Act, 2025 introduces a tabular format for TDS provisions, which is a major step toward simplification. The section contains three tables based on categories of payees:

- Residents

- Non-residents

- Any person

Each table clearly specifies:

- Nature of income or payment

- Applicable threshold limit

- Person responsible for deduction

- Applicable TDS rate

This structured approach replaces lengthy narrative provisions and makes compliance more straightforward and user-friendly.

No Major Change in TDS Rates and Thresholds

It is important to note that TDS rates and threshold limits remain largely unchanged under the new Act. The policy intent remains consistent with the earlier law. Taxpayers and deductors can continue relying on the same rates, subject to confirmation from the relevant provisions of the Income-tax Act, 2025 and the applicable Finance Act.

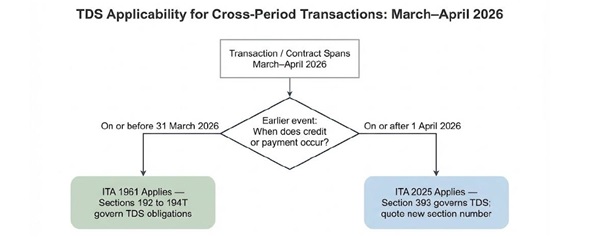

Applicability of TDS During Transition Period

The applicability of TDS provisions during the transition phase depends on the timing of payment or credit.

- If the amount is paid or credited on or before 31st March 2026, the provisions of the Income-tax Act, 1961 will apply

- If the amount is paid or credited on or after 1st April 2026, the provisions of the Income-tax Act, 2025 will apply

This ensures a clear distinction and avoids confusion during the transition period.

Source: Incometaxindia.gov.in

Requirement to Quote New Section References

For transactions undertaken on or after 1st April 2026, deductors and collectors must quote the relevant table item of Section 393 (for TDS) or Section 394 (for TCS) of the new Act. Continuing to use old section numbers such as 194C, 194J, or 194H may result in system validation errors, especially on the income tax portal. This makes it essential for taxpayers and professionals to update their compliance systems and documentation practices.

“Earlier of Credit or Payment” Rule Continues

The fundamental principle for TDS applicability—“earlier of credit or payment”—remains unchanged under the new Act.

- If the earlier event (credit or payment) occurs on or before 31st March 2026, TDS provisions of the old Act will apply

- If the earlier event occurs on or after 1st April 2026, TDS provisions under the new Act will apply

This continuity ensures that taxpayers do not face any ambiguity in determining TDS liability.

TDS Deposit Due Dates Remain the Same

The due dates for depositing TDS to the Government account continue to be governed by rules. Under the Income-tax Rules, 2026 (corresponding to earlier Rule 30), there is no change in timelines.

- General rule: TDS must be deposited by the 7th of the following month

- For March deductions (non-government deductors): Due date is 30th April

- For government deductors (challan cases): Due date is 7th April

Special cases such as property transactions, rent by specified individuals, and certain payments will continue to follow 30-day timelines, as applicable earlier.

Special Compliance for March 2026

TDS deducted in March 2026 will follow the old law timelines:

- Non-government deductors: Deposit by 30th April 2026

- Government deductors (challan mode): Deposit by 7th April 2026

Failure to comply with these timelines may attract interest and penalties, as per the applicable provisions.

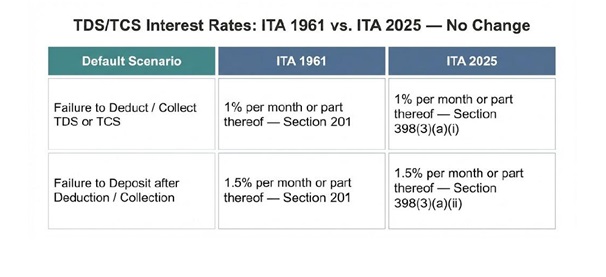

Interest on TDS Defaults Remains Unchanged

The provisions relating to interest on defaults in TDS/TCS remain unchanged under the Income-tax Act, 2025.

- Failure to deduct TDS/TCS: Interest at 1% per month or part thereof from the date it was deductible to the date of actual deduction

- Failure to deposit TDS/TCS: Interest at 1.5% per month or part thereof from the date of deduction to the date of payment

These provisions ensure continued discipline in compliance and timely deposit of taxes.

Source: Incometaxindia.gov.in

Final Words

The TDS framework under the Income-tax Act, 2025 reflects a perfect balance between continuity and simplification. While the core compliance structure, rates, and timelines remain unchanged, the presentation of provisions has been significantly improved through consolidation and tabular formats.

For taxpayers, businesses, and professionals, the key takeaway is that there is no need to relearn the system from scratch, but there is a need to adapt to the new structure and section references. The transition phase will require careful attention, especially in determining the applicable law based on timing and updating compliance processes accordingly.