Introduction

Let’s start with another blog on the new Income-tax Act, 2025, where we bring you the latest updates and practical insights on what is being introduced under the new law. Our aim is to cover each aspect in a simple and structured manner so that taxpayers get sufficient time to understand, plan, and implement the changes effectively. With the new Act coming into force from 1st April 2026, it is important to not only know the provisions but also understand their real implications on day-to-day compliance.

Continuity of Existing Systems: PAN, TAN & Faceless Proceedings

One of the biggest concerns among taxpayers is whether the current compliance systems will change. The good news is that existing frameworks such as Permanent Account Number (PAN), Tax Deduction Account Number (TAN), faceless assessments, and faceless appellate mechanisms will continue under the new law. This ensures that taxpayers and businesses do not have to go through the burden of adapting to an entirely new system. The continuity of these mechanisms reflects the government’s intention to ensure a smooth and stable transition.

Why Transitional Provisions Are Necessary

Taxation does not operate within strict yearly boundaries. While certain obligations like TDS, TCS, and advance tax payments occur within the financial year, many processes such as return filing, assessments, reassessments, appeals, penalties, and refunds extend beyond the year and sometimes continue for several years. Because of this, when a new law is introduced, it is not possible to completely replace the old law overnight. Both laws need to function simultaneously for a certain period to maintain continuity and avoid disruption.

Section 536: The Backbone of Transition

The Income-tax Act, 2025 addresses this transition through Section 536, which acts as a repeal and savings clause. This section contains multiple sub-clauses that deal with various practical scenarios arising during the transition. It ensures that the provisions of the old Income-tax Act, 1961 continue to apply to earlier tax years while aligning the framework with the new law. The purpose of this section is to modernize the law without disturbing established positions or creating confusion among taxpayers.

Protection of Taxpayer Rights and Benefits

An important feature of the transition is that all rights, benefits, obligations, and liabilities arising under the old Act will continue even after the new Act comes into force. For instance, if a taxpayer is eligible for a refund for any tax year prior to 1st April 2026, that right will remain intact. The taxpayer will continue to receive such benefits as per the provisions of the old law. This ensures that no taxpayer is adversely affected due to the change in legislation.

Treatment of Pending and Future Proceedings

As per the provisions of section 536(2)(c), all proceedings related to earlier years will continue to be governed by the old Act. This includes notices, assessments, reassessments, recomputations, rectifications, penalties, revisions, and appeals. Even if such proceedings are initiated after 1st April 2026, they will still be handled under the Income-tax Act, 1961 if they relate to earlier years. For example, an assessment for Assessment Year 2024–25 will be completed entirely under the old Act, ensuring procedural consistency.

Validity of Circulars and Notifications

Another key clarification under section 536(2)(j) is that all circulars, notifications, instructions, and approvals issued under the old Act will continue to remain valid, provided they are not inconsistent with the new law. This is particularly important for interpretation and practical application. For example, existing clarifications under TDS provisions will continue to apply under the corresponding provisions of the new Act where the intent remains the same. This avoids unnecessary confusion and ensures continuity in interpretation.

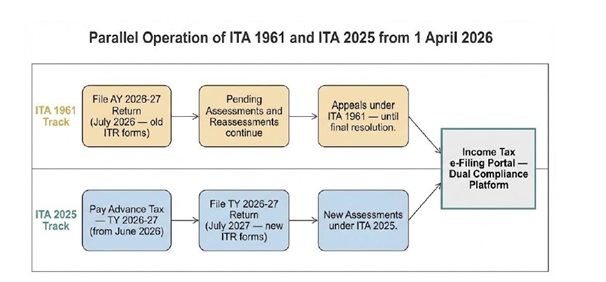

Simultaneous Operation of Old and New Laws

From 1st April 2026, the Income-tax Act, 1961 will be repealed. However, it will continue to apply to all tax years prior to this date. As a result, both the old and new laws will operate simultaneously for a certain period. The income tax portal will be equipped to handle compliance under both frameworks.

For instance, taxpayers filing returns for Assessment Year 2026–27 in July 2026 will do so under the old Act, as it relates to income earned before April 2026. At the same time, advance tax payments for Tax Year 2026–27, starting from June 2026, will be governed by the new Act. Similarly, all ongoing assessments and appeals relating to earlier years will continue under the old provisions until their completion.

Source: Incometaxindia.gov.in

Smooth Transition with Minimal Disruption

The transition to the Income-tax Act, 2025 has been carefully planned to ensure minimal disruption to taxpayers and professionals. By allowing both laws to coexist for a period, the government has ensured that there is no confusion or legal uncertainty. The systems, processes, and rights under the old law remain protected, while the new law gradually takes effect for future income.

Final Words

The introduction of the Income-tax Act, 2025 is not just a legal reform but a structured transition towards a simpler and more modern tax system. Through provisions like Section 536 and the continuation of existing frameworks such as PAN, TAN, and faceless proceedings, the government has ensured that the shift is smooth and taxpayer-friendly.

As we continue this blog series, we will break down each update in detail to help taxpayers understand the practical implications and prepare in advance. The focus is on making compliance easier, reducing confusion, and helping taxpayers confidently adapt to the new regime.